All About Debt Recycling

We're all looking for smart ways to get ahead financially. One strategy you might hear about is debt recycling. It sounds complex, but the fundamental idea is quite simple: you turn your 'bad' debt into 'good' debt. Let's break down what it is, how it works, and the things you need to watch out for.

What Is Debt Recycling?

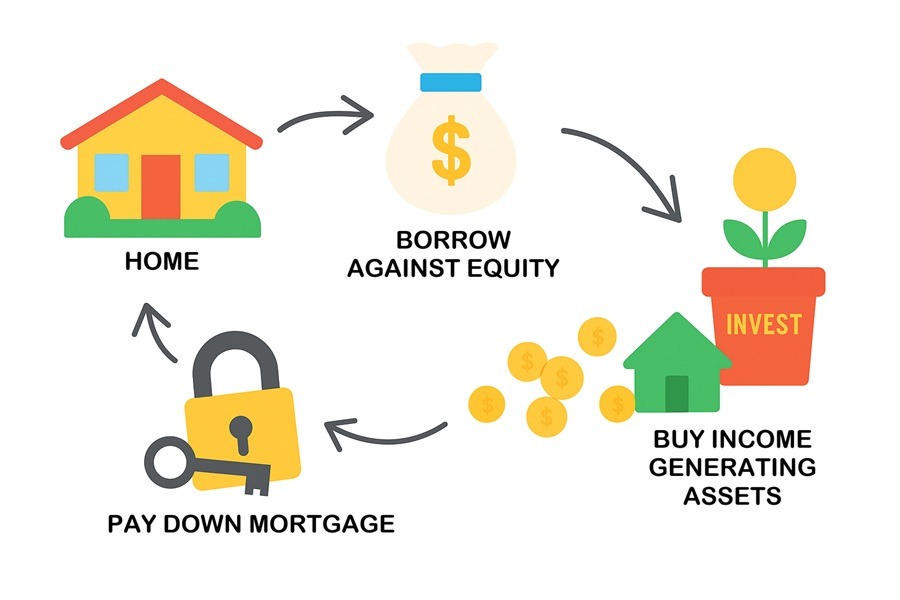

At its core, debt recycling is a strategy where you systematically pay down your home loan (which is typically non-deductible debt) and then redraw those funds to invest in assets that have the potential to produce income, like shares or property.

The magic of this process is that the interest on the money you've redrawn for investing can become tax-deductible. This is because the Australian Taxation Office (ATO) generally allows you to claim a deduction for expenses incurred while earning assessable income. So, you're effectively 'recycling' your home loan into a tax-friendly investment loan.

How Does It Work? A Step-by-Step Guide

The mechanics of debt recycling involve a few key steps. It's vital to set this up correctly to keep your deductible and non-deductible debts separate.

- Pay Down Your Home Loan: You start by making a principal payment into your home loan or offset account. For example, let's say you make a $10,000 lump-sum payment.

- Redraw the Funds: You then redraw that same amount ($10,000) from your loan. It is crucial that this redrawn amount is used only for investing.

- Invest: You use the $10,000 to purchase income-producing assets, such as a portfolio of dividend-paying shares.

- Claim the Deduction: The interest that accrues on that $10,000 portion of your loan is now generally tax-deductible. You must keep meticulous records to prove the funds were used for investment purposes. Tax savings and dividends can then be used to pay down your non-deductible home loan.

Over time, you can repeat this process, gradually converting your non-deductible home loan into a deductible investment loan and building a significant investment portfolio along the way.

The Main Benefits

Why go to all this trouble? There are two powerful advantages:

- A Bigger Asset Base: You're not just paying off a home loan; you're simultaneously building an asset base in shares or property. This gives you two assets (your home and your portfolio) growing in value, rather than just one.

- Tax Efficiency: By making some of your debt tax-deductible, you reduce your taxable income. This means you'll pay less tax, freeing up more cash that you can use to pay down your home loan even faster or to reinvest.

A Simple Illustration

Here’s a simplified look at how the numbers might stack up. Imagine you have a $500,000 home loan and $20,000 in savings.

| Scenario | 1. Without Debt Recycling | 2. With Debt Recycling |

| Home Loan | $480,000 (after paying down $20k) | $500,000 |

| Investment Loan | $0 | $20,000 (split from home loan) |

| Total Debt | $480,000 | $500,000 |

| Deductible Debt | $0 | $20,000 |

| Investment Portfolio | $0 | $20,000 |

In the second scenario, while the total debt is higher initially, a portion of it is now working for you by funding an investment and providing a tax deduction.

What Are the Risks?

This strategy doesn't come without risks, and it's important to be aware of them.

- Market Fluctuations: The value of your investments can go down as well as up. If your portfolio performs poorly, you could be left with a large debt and assets that are worth less than you paid for them.

- Interest Rate Changes: If interest rates rise, the cost of your investment loan will increase, eating into your returns.

- Records Management: Debt recycling requires careful management and good record-keeping. Mixing personal and investment funds can create a mess that's difficult to sort out, especially with the tax office.

Is It Right for You?

Debt recycling can be a powerful wealth-creation tool, but it's not for everyone. It generally suits those who have a stable income, a long-term investment horizon, and a good tolerance for risk.

Before you consider a strategy like this, it's important to get professional financial advice. A qualified adviser can help you understand if it aligns with your personal circumstances and financial goals, and ensure you set it up correctly from the start. So make sure you speak to us before considering this strategy.